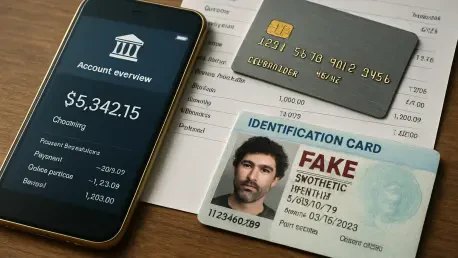

The quiet emergence of a phantom customer who possesses a valid social security number but has no physical existence represents one of the most sophisticated challenges facing the modern global financial ecosystem today. As digital banking platforms continue to prioritize seamless user experiences and rapid onboarding, criminal enterprises have shifted their focus from simple identity theft to the creation of entirely fabricated personas. These synthetic identities are not stolen in the traditional sense; rather, they are assembled like puzzles, blending genuine government-issued identifiers with fictitious personal data. This evolution in financial crime has caught many neobanks and traditional lenders off guard, as their legacy detection systems are often calibrated to flag inconsistencies in real identities rather than the polished, consistent perfection of a synthetic profile. The financial sector currently finds itself in an arms race where the weapon of choice is no longer just stolen data, but the strategic manufacturing of credibility within the credit reporting system itself.

1. The Complex Nature of Synthetic Identity Construction

Synthetic identity fraud fundamentally differs from traditional third-party fraud because it does not involve the total takeover of a living person’s account or identity. Instead, perpetrators engage in a “Frankenstein” method of identity creation, where a legitimate Social Security Number (SSN)—often belonging to a child, an elderly individual, or a deceased person—is combined with a false name, a secondary mailing address, and a specific birth date. Because these SSNs are frequently “dormant,” meaning they have no existing credit history or active digital footprint, they provide a clean slate for fraudsters to exploit. This lack of a victim who monitors their credit report means the fraud can persist for years without detection, unlike traditional identity theft where the real owner of the credentials would likely notice unauthorized charges or changes to their credit score almost immediately.

The primary challenge for digital banks lies in the fact that these manufactured personas often look like ideal customers on paper. By utilizing SSNs that have never been associated with a credit file, criminals can bypass the usual red flags that indicate a stolen identity, such as mismatched addresses or previous delinquency records. These identities are meticulously nurtured to appear as “thin-file” customers—individuals who are simply new to the credit market, such as recent immigrants or young adults. Because digital lenders are often eager to capture this demographic, they may inadvertently lower their defensive barriers to facilitate growth. This structural vulnerability has allowed synthetic fraud to become one of the fastest-growing categories of financial crime, as the lack of a clear, immediate victim makes it remarkably difficult for automated systems to distinguish between a legitimate new borrower and a sophisticated criminal construct.

2. The Strategic Lifecycle of a Manufactured Persona

The process of bringing a synthetic identity to life is a patient and methodical endeavor that often spans several months or even years. It begins with the acquisition of a high-quality SSN, which is typically sourced from dark web marketplaces that specialize in unassigned or dormant government identifiers. Once a suitable number is secured, the fraudster establishes a basic digital presence by creating social media accounts, registering email addresses, and obtaining a Voice over IP (VoIP) phone number. The first interaction with the financial system usually involves applying for a small, unsecured credit product or a retail store card. While the initial application is almost always rejected because no credit file exists for that name and SSN combination, the act of applying forces the credit bureaus to generate a new credit header, effectively “birthing” the synthetic identity into the formal financial record.

After the identity has been officially recognized by the credit bureaus, the fraudster enters the “seasoning” phase, where they gradually build a positive credit history to increase the identity’s borrowing power. This is often achieved through “piggybacking,” where the synthetic persona is added as an authorized user to a legitimate credit account with a long history and high limit. Once the synthetic identity’s credit score has been artificially inflated, the perpetrator begins applying for progressively larger loans, credit cards, and lines of credit from multiple digital banks. The lifecycle culminates in a “bust-out,” a coordinated event where the fraudster maxes out all available credit limits simultaneously across several institutions. By the time the bank realizes the payments have stopped, the perpetrator has vanished, leaving the institution to write off the loss as a standard credit default rather than recognizing it as a targeted fraudulent attack.

3. Technological and Social Drivers of Modern Fraud Growth

The rapid expansion of synthetic identity fraud is fueled by a perfect storm of massive data availability and the democratization of advanced technological tools. Major data breaches over the past few years have flooded the market with hundreds of millions of personal records, providing criminals with an inexhaustible supply of legitimate SSNs to serve as the foundation for synthetic builds. Furthermore, the competitive nature of the digital banking sector has led many institutions to implement frictionless onboarding processes that prioritize speed above all else. While these “one-click” applications are excellent for customer acquisition, they often rely on static data verification that is easily bypassed by high-quality synthetic identities. When speed is the primary metric for success, the thoroughness of identity verification inevitably suffers, creating an opening that organized crime groups are more than willing to exploit.

Moreover, the arrival of generative artificial intelligence has fundamentally altered the landscape by allowing fraudsters to scale their operations with unprecedented realism. Sophisticated AI models can now generate lifelike profile pictures, create convincing employment histories, and even simulate human-like behavior on mobile banking apps. These tools enable criminals to produce the diverse array of “evidence” required to pass modern Know Your Customer (KYC) checks, such as fake utility bills or synthetic driver’s licenses that are virtually indistinguishable from the real thing. As AI-driven automation continues to lower the cost of creating these identities, digital banks are seeing a surge in high-volume attacks that can overwhelm manual review teams. The ability of generative technology to mimic the nuances of human interaction makes it increasingly difficult for institutions to rely on traditional behavioral patterns as a defensive measure.

4. Operational and Financial Consequences for Institutions

For financial institutions, the impact of synthetic identity fraud extends far beyond the immediate loss of capital associated with a bust-out event. Estimates suggest that U.S. lenders lose billions of dollars annually to this specific form of crime, with a significant portion of these losses being misclassified as “bad debt” or traditional credit defaults. When a bank fails to identify a synthetic identity at the point of entry, the resulting financial damage is often much higher than in other types of fraud because the criminal has had time to secure large, unsecured personal loans or high-limit credit cards. These losses directly affect the bottom line and can lead to higher interest rates for legitimate consumers as banks seek to offset their increased risk. The financial strain is compounded by the fact that recovering funds from a non-existent person is an impossible task for collections departments.

Beyond the direct monetary hit, digital banks face severe regulatory scrutiny and potential damage to their reputations. Regulators are increasingly holding institutions accountable for their failure to detect synthetic personas, viewing it as a lapse in Anti-Money Laundering (AML) and KYC compliance. A high rate of synthetic fraud can trigger intensive audits, resulting in heavy fines and mandated changes to onboarding workflows that may hinder a bank’s ability to compete. Additionally, the presence of synthetic identities in a bank’s portfolio pollutes the data used for credit modeling and risk assessment. If a bank’s algorithms are trained on data that includes fraudulent accounts that “behaved” well for a year before busting out, the resulting credit models will be flawed, leading to poor lending decisions in the future. This degradation of data integrity presents a long-term strategic risk that can take years to rectify.

5. Primary Indicators of Synthetic Fraud During Onboarding

Identifying a synthetic identity requires a shift in focus toward subtle discrepancies that appear during the initial application process. One of the most common red flags is a significant mismatch between the age of the SSN and the age of the applicant; for example, an SSN issued in the early 2000s belonging to an applicant claiming to be in their fifties is a clear sign of potential synthetic activity. Banks have also begun to monitor for suspicious patterns in physical addresses, such as multiple applications originating from a single high-density apartment complex or the use of commercial mail drops that are disguised as residential suites. Forensic document inspection has become equally critical, as many synthetic identities rely on digitally altered paperwork that may appear perfect to the naked eye but contains metadata inconsistencies or font anomalies that are detectable by automated scanning tools.

Furthermore, the behavioral signatures of synthetic applicants often differ from those of genuine customers in ways that are difficult to fake. A person who is manually entering data they have memorized will type differently than a bot or a professional fraudster who is copying and pasting information from a database. Automated systems can now detect “perfect” credit files that lack any of the typical “noise” found in a real person’s history, such as old addresses, varying name spellings, or a mix of good and bad credit markers. Real human credit files are messy; synthetic files are often suspiciously clean and logical. Additionally, duplicate device fingerprints or IP addresses that link seemingly unrelated applications can reveal the presence of a fraud ring operating behind the scenes. By correlating these technical and behavioral signals, digital banks can begin to strip away the mask of legitimacy that synthetic personas wear.

6. Advanced Strategies for Identifying Synthetic Personas

To combat the rise of manufactured identities, leading digital banks are moving toward a multi-layered defense strategy that emphasizes real-time behavioral analysis and cross-industry collaboration. Behavioral biometrics have emerged as a powerful tool, as they analyze the unique way a user interacts with their device—ranging from screen pressure to the angle at which the phone is held. Because these physical behaviors are nearly impossible for a bot or a distant fraudster to replicate perfectly, they provide a strong signal of liveness and authenticity. Additionally, advanced liveness checks during the selfie-verification phase are being used to ensure that a real human is present at the time of application, effectively countering the use of static deepfakes or high-quality masks that were common in previous years.

Graph analysis and data sharing across the financial industry have also proven to be essential in mapping the hidden connections that define fraud rings. By participating in shared fraud databases, banks can see if a specific SSN or phone number has been used in suspicious applications at other institutions, even if the names on those applications were different. Graph technology allows investigators to visualize how seemingly disparate accounts are linked through shared attributes like a common IP address, a recurring physical location, or a similar sequence of credit-building actions. This holistic view of the threat landscape enables banks to move from a reactive posture to a proactive one, identifying and blocking synthetic identities before they have a chance to establish a foothold. Ongoing account surveillance is equally vital, as monitoring for sudden, dramatic changes in spending behavior months after an account was opened can flag a “bust-out” in progress.

7. Critical Recommendations for Enhancing Identity Verification

Industry leaders recognized that the most effective path forward involved a total departure from static verification methods in favor of dynamic, risk-based onboarding. By categorizing applicants into different risk tiers at the moment of initial contact, institutions were able to apply more rigorous forensic scrutiny to high-risk profiles while maintaining a frictionless experience for established customers. This approach required the adoption of a zero-trust identity policy, where no single piece of data was accepted as proof of existence without secondary, independent corroboration from disparate sources. These measures were supplemented by the implementation of AI-powered screening tools that could analyze millions of data points in milliseconds to spot emerging fraud patterns that would be invisible to human reviewers.

The most successful prevention strategies also emphasized the human element, as banks invested heavily in specialized training for their fraud and legal departments to interpret the subtle signals generated by automated systems. Financial institutions formed robust professional coalitions to share intelligence on the latest tactics used by international fraud syndicates, creating a collective defense that made it significantly more expensive for criminals to operate. Furthermore, banks moved to integrate direct verification links with government databases, allowing for real-time confirmation of SSN and name matches at the source. These comprehensive changes turned the tide against synthetic identity fraud, transforming what was once a silent threat into a manageable risk that could be identified and mitigated through technological precision and industry-wide cooperation.